The question often arises with a sense of urgency: "Is now a good time to invest?" While understandable, this framing may be misleading. The more constructive answer has less to do with the market's daily movements and more to do with an individual's personal circumstances.

While headlines report on market highs and lows, experienced investors understand that the most reliable signals come from a well-considered financial plan, not from forecasting market behavior.

Reframing the Question About When to Invest

It is natural to seek a simple "yes" or "no" before committing capital. This desire often emerges during significant financial moments—perhaps following a market downturn, or upon receiving funds from the sale of a business or an inheritance.

The challenge with focusing on market timing is the attempt to control an inherently uncontrollable variable. Consistently predicting short-term market direction is a task that eludes even dedicated professionals. A more effective approach is to turn the question inward.

From Market Timing to Personal Readiness

Instead of asking if it is a good time for the market, consider whether it is the right time for you. This shift in perspective moves the focus from speculation to strategic planning.

Your personal readiness is the true indicator. It requires a clear understanding of your own financial foundation.

This readiness can be assessed through three key areas:

- Your Investment Horizon: How long can this capital remain invested before you require access to it? A 35-year-old professional saving for retirement is operating on a different timeline than a 60-year-old preparing to generate income from their portfolio.

- Your Financial Stability: Is a sufficient emergency fund in place? Have high-interest debts been addressed? Attempting to build a portfolio on an unstable financial base can lead to difficult decisions during periods of market volatility.

- Your Long-Term Goals: What is the purpose of this capital? Is it intended to fund a child’s education, secure your own retirement, or establish a legacy for future generations? The "why" behind the investment should always inform the "how."

The following table may help reorient your focus away from market noise and toward what is personally relevant.

Shifting Focus From Market Timing to Personal Readiness

| Common Market-Focused Question | A More Thoughtful Personal Question |

|---|---|

| Is the market too high (or too low) right now? | Do I have a clear financial plan, and is this investment consistent with it? |

| What will interest rates do next? | Have I addressed high-interest debt and established an adequate emergency fund? |

| Should I wait for the next market downturn to invest? | What is my time horizon for this capital, and can I tolerate normal market fluctuations? |

| Which investment will perform best next year? | What specific life goal am I investing for, and what is the appropriate strategy? |

By shifting your mindset, you recognize that control lies not in predicting the future, but in preparing for it based on your unique circumstances.

By focusing on these personal elements, you can build a framework for making sound decisions with confidence, regardless of market commentary. The goal is to act from a position of preparedness, not in reaction to noise. This approach fosters discipline and patience—two critical components of long-term investing success.

Time in the Market vs. Timing the Market

A foundational concept that distinguishes a strategic investor from a speculator is the principle of "time in the market versus timing the market." The former is a disciplined strategy for growth; the latter is an exercise in prediction.

The appeal of market timing is undeniable. The prospect of selling at a peak and repurchasing at a bottom is attractive. However, history shows this is nearly impossible to execute consistently, even for professional fund managers.

Attempting to time the market requires being correct twice: on the exit and on the re-entry. More often, it leads to missed opportunities and suboptimal outcomes.

Compounding: The Quiet Engine of Growth

The power of long-term investing lies not in selecting the perfect day to buy, but in the process of compounding—where your investment returns begin to generate their own returns. This effect requires one critical ingredient: time.

By remaining invested through the market's inevitable cycles, you allow your capital the uninterrupted period it needs to grow. What might appear as a significant downturn today often registers as a minor fluctuation on a multi-decade chart.

This long-term perspective is also a defense against emotional decision-making. When you understand that consistent participation is a key driver of results, you can observe market volatility with composure rather than alarm.

A long-term perspective rewards patience far more than it rewards prediction. The objective is not to sidestep every downturn but to build a resilient plan that can endure them, allowing your assets the uninterrupted time they need to grow.

Building a Durable Investment Philosophy

This is how a financial plan is constructed to withstand changing conditions. It begins with acknowledging a simple truth: markets are unpredictable in the short term, but over the long term, they have historically reflected the progress of economic growth and human innovation.

Committing to "time in the market" is an expression of confidence in that long-term progress.

It is a calmer, more intentional path. Instead of reacting to every headline, you align your actions with your personal timeline and goals. This allows you to build a strategy designed not just for the next quarter, but for the years and decades to come.

How Your Personal Timeline Shapes Investment Strategy

An effective investment strategy is a reflection of your life, not the daily movements of the market. The single most important factor is your investment horizon—the length of time until you will need to access the funds.

This timeline dictates nearly every other aspect of the strategy. It informs the appropriate level of risk, the balance between growth and preservation, and the types of assets to consider. This is why "is now a good time to invest?" is always a personal question. A suitable action for one person could be inappropriate for another, even if they are investing on the same day. The market provides the context, but your timeline provides the direction.

Contrasting Timelines: Two Scenarios

Consider two individuals, both prudent with their finances. Their optimal paths diverge based on their age and goals.

The Professional in Their Early 40s: This person has decades before retirement. Their primary objective is long-term growth. With ample time to recover from market downturns, their portfolio can be structured to emphasize assets with higher growth potential. A period of poor performance is unlikely to derail a 20- to 30-year plan.

The Pre-Retiree in Their Late 50s: For this investor, retirement is approaching. The focus shifts from aggressive growth to capital preservation and establishing a reliable income stream. A significant market decline just before they cease working could have a material impact on their plans. Their strategy must be more conservative, balancing modest growth with greater stability.

This comparison illustrates a core principle of investing.

The longer your time horizon, the more volatility you can typically withstand in pursuit of higher long-term returns. As you approach your destination, the priority shifts toward preserving the wealth you have accumulated.

Aligning Your Strategy with Your Horizon

This way of thinking can liberate you from the distraction of market predictions. For the professional in their 40s, nearly any time is a suitable time to be investing consistently. Decades of compounding have a way of smoothing out market fluctuations.

For the pre-retiree, however, the decision is more nuanced. They might need to phase into investments gradually or begin with a more defensive asset allocation.

When you understand your timeline, the vague question "Is it a good time to invest?" transforms into a clearer, more practical one: "Given my personal situation, what is a prudent way to deploy capital today?" This perspective also influences other areas of your financial life, including taxes. For more on that topic, you can review our thoughts on how to reduce taxable income.

Understanding the Broader Economic Landscape

A sound financial plan is centered on your personal goals and timeline. However, it does not exist in a vacuum. It is prudent to maintain an awareness of the wider economic environment—not to react to every headline, but to understand the context in which your strategy operates.

Think of it as checking the weather before a long journey. A forecast of rain doesn't cancel the trip, but it might prompt you to pack appropriate gear. The goal is similar: to appreciate how a well-constructed portfolio is designed for resilience, regardless of the economic climate.

Interpreting Key Economic Signals

A deep knowledge of economics is not a prerequisite for successful investing. Much of the financial news centers on a few key signals that can influence asset values. Understanding them in simple terms helps to clarify the discourse.

Consider two of the most frequently discussed factors: interest rates and inflation.

Interest Rate Environments: When a central bank raises interest rates, it becomes more expensive to borrow money. This tends to have a cooling effect on the economy and can make lower-risk investments like bonds appear more attractive relative to equities. Conversely, low interest rates can stimulate economic activity and support stock market performance.

Inflation Trends: Inflation gradually erodes the purchasing power of cash. If inflation is 3%, your capital must grow by more than 3% just to maintain its real value. A primary objective of investing is to outpace inflation over the long term. Historically, assets like equities and real estate have been more effective at this than cash or long-term bonds.

A thoughtfully diversified portfolio already accounts for these forces. It is built to navigate different economic seasons, balancing assets that may perform well in one environment with those that may perform well in another. This is why a disciplined approach tends to be more reliable than attempts at economic forecasting.

This is a core reason why we advocate for adhering to a strategy rather than engaging in speculation. For further discussion on how we navigate different market conditions, feel free to explore our investment viewpoints.

Seeing Through the Headlines

It is also important to look beyond prominent headline figures. Often, the more meaningful story lies in the details.

For example, a report might show that global foreign direct investment has increased significantly, suggesting a robust global economy. However, a deeper analysis might reveal that much of this increase is due to capital flows between international financial centers, rather than new investment in productive assets. You can read more about these global investment trends from UNCTAD to see this nuance.

For a long-term investor, that detail is significant. It serves as a reminder that understanding where capital is actually being deployed is more insightful than a single headline number.

Ultimately, your awareness of the economic landscape should provide context for your plan, not dictate it. It helps you remain informed without being diverted from your disciplined, long-term decisions.

Navigating Divergent Global Market Performance

It is a common tendency, even for experienced investors, to favor familiar markets. When one's domestic stock market has performed well for an extended period, it can be tempting to concentrate investments there.

However, this perspective overlooks a crucial aspect of global economics. Market leadership is rarely permanent; it tends to rotate among different regions over time.

Markets around the world do not always move in unison. Different economies are driven by their own cycles, industries, and demographic trends. By concentrating a portfolio in a single country, an investor is implicitly betting that its outperformance will continue indefinitely. This is a difficult proposition to win over the long haul.

The Case for Geographic Diversification

Building a globally diversified portfolio is an acknowledgment that it is impossible to know with certainty which country's economy will lead in the coming decade. Instead of guessing, you position yourself to participate in growth wherever it may occur.

This approach can act as a shock absorber for a portfolio. When one region is experiencing difficulty, another may be thriving, which can help to smooth overall returns. It is a more measured strategy than chasing the "hot" market of the moment, a practice that often leads to buying high and selling low.

The dynamic between developed and emerging markets illustrates this point. There are periods where diversification proves its value as different regions outperform. Yet forecasts can change quickly, highlighting the difficulty of timing these shifts. You can explore global equity projections and the case for diversification for a deeper analysis.

A well-structured portfolio is not about making a single, concentrated bet on one economy. It is about assembling a collection of global assets that work in concert, creating a resilient structure designed to endure various economic conditions.

The objective is not to perfectly predict which region will lead next, but to build a portfolio that is positioned to benefit from global progress over the long term. By diversifying investments across the globe, you make your financial future less dependent on the fortunes of any single nation. It is a core principle of evidence-based investing.

A Personal Framework for Your Decision

After considering your timeline, the economic climate, and global market dynamics, the decision returns to your personal situation. The central question is not simply "is it a good time to invest?" but rather, "is it the right time for me to invest?" This requires a clear-eyed assessment of your own circumstances.

A structured approach can help you move past emotional noise and toward clarity. Before committing capital, it is wise to address a few foundational questions. Honest answers will provide the confidence needed to adhere to a long-term plan, regardless of short-term market behavior.

Key Questions for Your Reflection

Consider these the pillars of your financial life:

What is the purpose of this capital? Is it for retirement in 20 years? A down payment in five? A child’s education in a decade? The purpose defines the strategy.

What is my genuine time horizon? How long can you realistically leave this money invested without needing to access it? A longer horizon allows for a different approach to risk.

What are my liquidity needs? Do you have a sufficient emergency fund, entirely separate from your investments? A solid financial foundation enables confident investing.

How does this fit within my overall plan? Is this investment consonant with your other financial activities, including tax and estate planning?

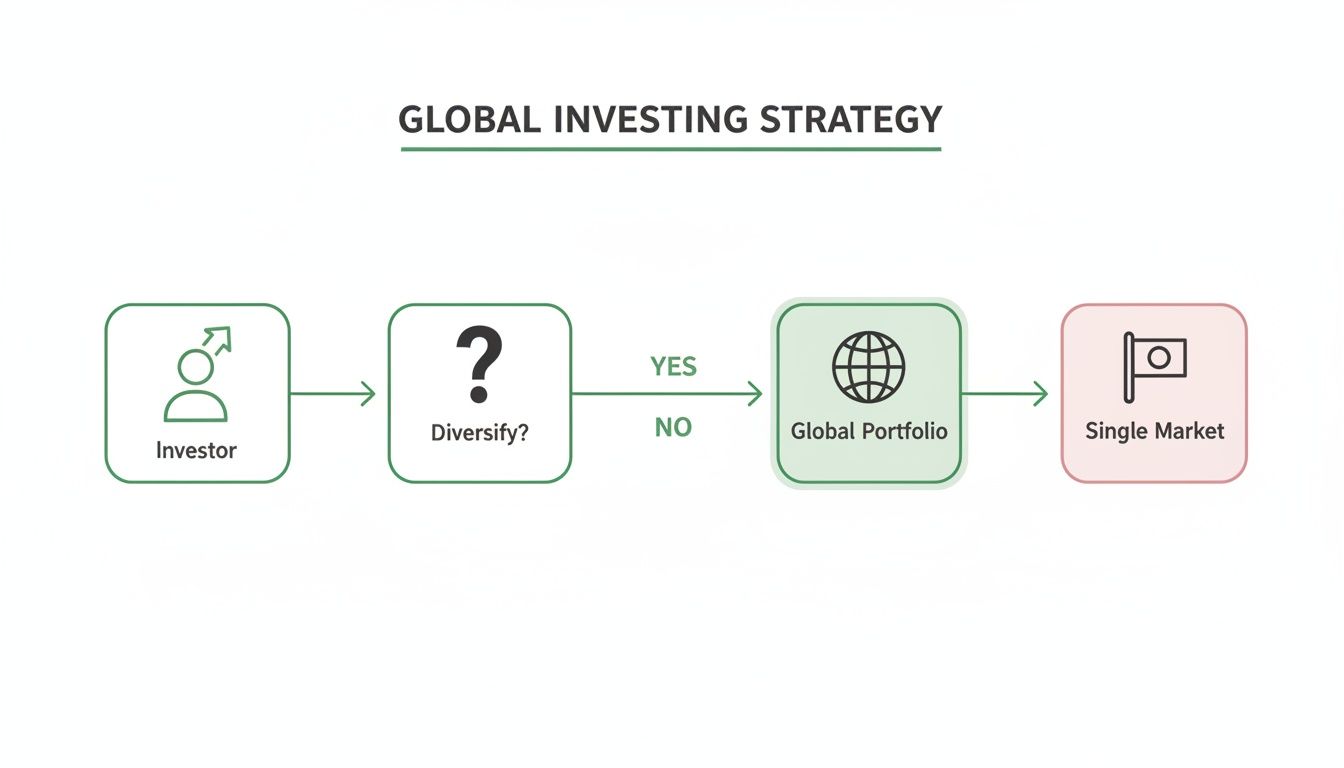

The flowchart below illustrates one of the fundamental strategic choices in portfolio construction: the approach to global diversification.

While a simple visual, it emphasizes a critical point: high-level strategic decisions like this will have a far greater impact on your long-term success than attempting to perfectly time your entry into the market.

The purpose of this framework is not to find a single perfect answer. It is to ensure you are asking the right questions. A thoughtful process is always more valuable than a fortunate guess.

If you find these questions complex or are uncertain about the answers, it may indicate that objective guidance could be beneficial. A fiduciary advisor can help bring clarity to how these pieces fit together, ensuring your decisions are aligned with your best interests. This is particularly relevant for those nearing or in retirement, where effective portfolio management for retirement is essential.

Answering Your Lingering Questions

Even with a well-considered plan, certain questions can surface just as you prepare to act. Addressing these common concerns can provide the confidence needed to stay the course.

"Should I Wait for the Market to Go Down Before I Invest?"

The idea of "buying low" is appealing. However, attempting to identify the precise bottom of a market cycle is exceptionally difficult.

The greater risk is often remaining on the sidelines, waiting for a perfect entry point that may not materialize. During this waiting period, you could miss significant market gains. A more dependable approach is to invest when your financial plan indicates you are ready. A sound, long-term strategy is designed to navigate the market's natural cycles, capturing growth over years, not just timing the next few months.

"But What if I Invest Right Before a Major Downturn?"

This is an understandable concern. The thought of investing a significant sum just before a market decline is unsettling, even for experienced professionals.

If this is a primary concern for you, a strategy known as dollar-cost averaging may be appropriate. Instead of investing a large lump sum at once, you can divide it into smaller, regular investments over a set period.

This approach mitigates the risk of committing all your capital at a single price point. By investing consistently, you average out your purchase price over time. It can be an effective way to manage emotional responses during periods of market volatility.

"How Do I Know if I'm Personally Ready to Invest?"

This is the most important question. The true signal to invest comes from your own financial stability.

Before proceeding, ensure a few foundational elements are in place:

- You have a stable and reliable source of income.

- You have established an emergency fund to cover 3-6 months of essential living expenses.

- You are not burdened by high-interest debt, such as credit card balances.

If you have met these conditions and have clear long-term goals, then your personal "right time" may be now. This solid foundation is the most reliable indicator that you are prepared to begin building long-term wealth.

At Wealth Accel, our role is to provide objective guidance to help you answer these questions with confidence. If you are ready to build an investment strategy that is aligned with your personal circumstances, we invite you to connect. You can schedule a conversation with us to begin the discussion.

Created with Outrank