For a business owner, planning your estate is a defining act of leadership. It moves beyond a standard financial exercise to address the fundamental continuity of the enterprise you have built. The process requires a distinct perspective, one that considers how to safeguard a legacy deeply connected to your personal identity, your family’s future, and your community. Your business, after all, is more than an asset on a balance sheet.

Why Estate Planning Is a Unique Discipline for Entrepreneurs

Most estate planning focuses on the distribution of personal assets like a home, investments, and personal effects. For an entrepreneur, however, the lines between personal and business wealth are often intertwined. Your company is likely your most significant asset, but it also represents a source of purpose, the livelihood for your team, and the foundation for your family’s well-being.

This reality raises a series of questions that a typical estate plan is not equipped to answer. Who has the authority to lead the company if you are unexpectedly unable to? How can ownership be transferred without disrupting operations or creating conflict among family members and partners? A thoughtful estate plan for business owners provides clear, considered answers to these essential questions.

Protecting the Continuity of Your Work

The absence of a plan is, in itself, a decision—one that defers critical outcomes to the courts and chance. This is a significant consideration, given the number of businesses poised for a change in leadership. One study noted that 2.9 million businesses in the U.S. are owned by individuals aged 55 or older, collectively employing over 32 million people.

Furthermore, an estimated 73% of privately held companies are expected to transition ownership in the coming decade, putting approximately $14 trillion in assets in motion. Yet, a large number of owners are not adequately prepared for this transition. You can gain further perspective on this generational shift from research by Project Equity.

Planning for your business’s future is a core responsibility. It is the mechanism by which you ensure the continuity of your life's work, secure your family’s financial standing, and provide stability for the employees who rely on the enterprise.

A well-conceived estate plan is your final strategic decision. It replaces ambiguity with clarity, ensuring the principles that guided your business’s growth continue to shape its future.

The Value of Deliberate Planning

Ultimately, the objective is to facilitate a controlled, intentional transfer of leadership and ownership that aligns with your long-term vision. This requires more than legal documentation; it demands a careful examination of family dynamics, company culture, and your personal definition of success. It is an acknowledgment that this transition is as much an emotional journey as it is a financial one.

By addressing these challenges with foresight, you establish a sense of control and composure. A well-designed plan allows you to look toward the future with confidence, knowing your legacy is protected and positioned to endure.

The Foundational Documents of a Business Owner's Estate Plan

A durable estate plan is not a single document but a carefully integrated set of legal instruments. Each is designed for a specific purpose, working in concert to ensure your intentions are executed precisely. For a business owner, these documents require an additional layer of detail to delineate between personal assets and business interests.

While every situation is unique, the conversation typically begins with several key documents. Understanding their respective roles is the first step toward building a plan that can withstand future complexities.

The Distinct Roles of Wills and Trusts

The terms "will" and "trust" are often used interchangeably, but they serve very different functions. A Last Will and Testament is a legal document that outlines the distribution of your property and designates guardians for minor children upon your death. Its primary limitation is that it must pass through probate.

Probate is a court-supervised process that can be slow, public, and costly. For a business owner, this presents a significant challenge. Relying solely on a will can bring business operations to a standstill while awaiting court approval. Lenders, partners, and key employees are left in a state of uncertainty, potentially for months, until a judge validates the will and formally recognizes the new owner's authority.

A trust offers a solution. It is a private legal arrangement where you appoint a "trustee" to hold and manage assets for your beneficiaries. By placing your business ownership into a trust, you can bypass probate and facilitate a seamless, immediate transition of control.

- A Revocable Living Trust is a common choice for business owners due to its flexibility. You can amend it at any time. While you are alive and capable, you serve as the trustee, maintaining full control. If you become incapacitated or pass away, your designated successor trustee steps in without court intervention, allowing the business to continue without interruption.

- An Irocable Trust is a more permanent structure. Once assets are transferred into it, you generally cannot reclaim them or alter the terms. This approach is often used as a sophisticated strategy to protect assets from creditors and, importantly, to reduce estate taxes by removing the business from your taxable estate.

The appropriate choice depends on your objectives for control, flexibility, and tax efficiency. Many comprehensive plans utilize both: a trust for major assets like the business, and a will to address personal property and name guardians.

The Buy-Sell Agreement: A Framework for Transition

If a trust is the vehicle for transferring ownership, the Buy-Sell Agreement is the engine that governs the process. This is a legally binding contract among co-owners that dictates what happens to a partner's equity upon their departure—whether due to death, disability, retirement, or another triggering event.

A Buy-Sell Agreement can be thought of as a prenuptial agreement for business partners. It compels stakeholders to address difficult questions in advance, establishing clear rules before a crisis occurs.

This document serves as a roadmap for navigating a transition. It answers critical questions before they can create instability:

- Who has the right to purchase the shares? The agreement may grant remaining owners the first right of refusal, require the company to redeem the shares, or permit a transfer to a specific family member.

- What is the valuation method? To prevent disputes, a valuation formula is established beforehand. This could be a fixed price, a multiple of earnings, or a defined process for obtaining a professional appraisal, ensuring a fair price for the departing owner or their estate.

- How will the purchase be funded? The agreement can specify the funding mechanism, such as life or disability insurance policies, company cash flow, or a structured installment plan.

Without a buy-sell agreement, your partners could find themselves in business with an heir who lacks experience, or your family could be forced to sell your interest for a fraction of its value. It is a foundational tool for stability.

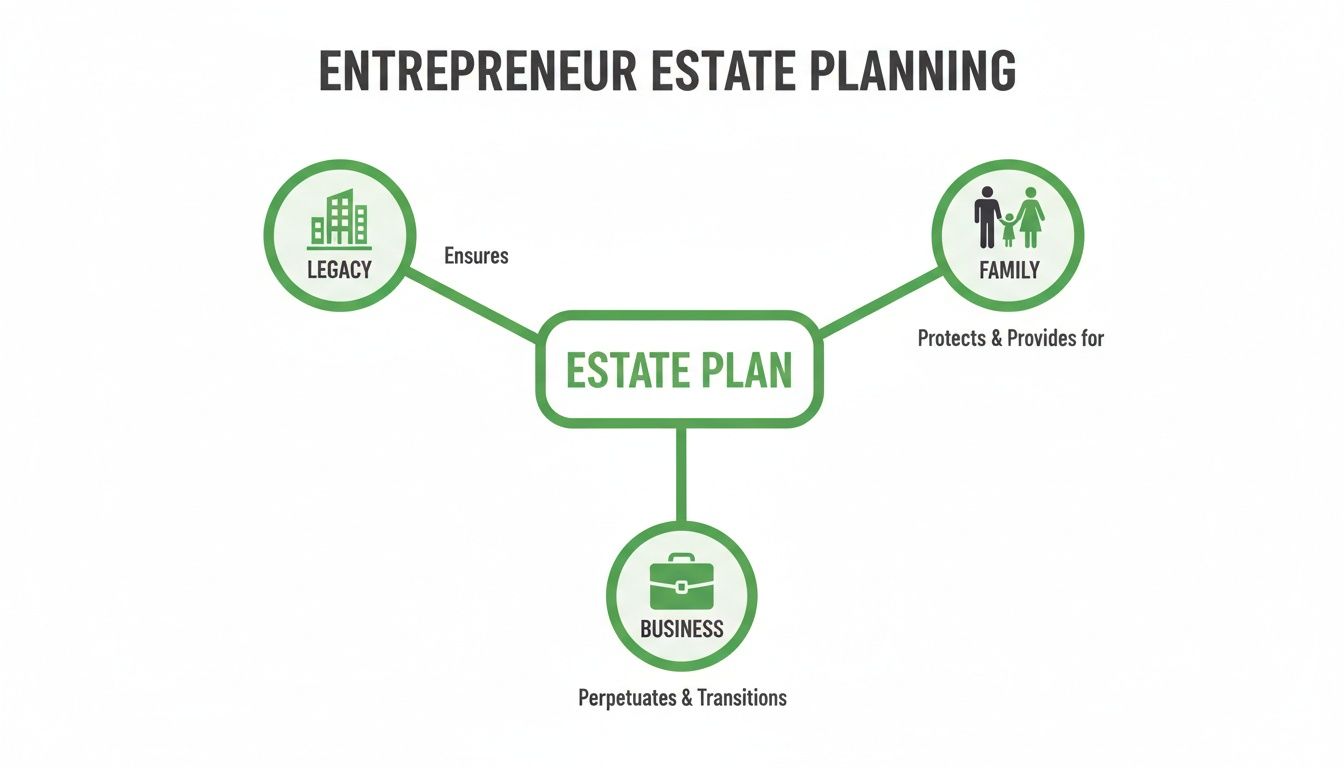

The graphic below illustrates how these documents create a structure connecting the three pillars of your life: your legacy, your family, and your business.

This demonstrates that an effective plan is not merely a collection of legal documents. It is a cohesive strategy that honors your commitments to your family while preserving the enterprise you built.

Connecting Succession Strategy to Your Estate Plan

For many entrepreneurs, contemplating life after the business can feel abstract. However, your estate plan is incomplete without a well-defined succession strategy. These are not separate endeavors; they are two sides of the same coin. A coherent strategy for one reinforces the other, creating a single, integrated roadmap for the future of your life's work.

This is more than a financial transaction. It is a personal journey that touches upon your identity, your family’s future, and the culture of the company you created. The objective is to move from a vague notion of what might happen "someday" to a documented plan that provides clarity and security for all involved.

Aligning Your Vision with a Viable Path

The first step is to reflect on what you truly want for the business when you are no longer leading it. There is no single correct answer. The best path depends on your values, your family circumstances, and your vision for the company's legacy.

Consider the most common pathways:

- Family Transfer: Passing the business to the next generation is a powerful way to continue a family legacy. This path requires years of intentional preparation, not only in training successors but also in navigating emotional complexities and ensuring fair treatment among all heirs, particularly those not involved in the business.

- Management Buyout (MBO): Selling to key employees can be an excellent option. It preserves the company culture and rewards the individuals who helped you build the enterprise. The primary challenge is typically financial, requiring the management team to secure adequate funding for the purchase.

- Third-Party Sale: An outright sale to an external buyer generally yields the highest valuation and offers a clean exit. The trade-off is a loss of control over the company's future direction and culture. The right choice depends on whether your priority is maximizing financial return or preserving a specific legacy.

Each option presents its own trade-offs. A family transfer might prioritize continuity over purchase price, while a third-party sale often does the opposite. Your estate plan must be structured to support your chosen path, ensuring the necessary legal and financial mechanisms are in place. For more on the agreements that facilitate these transitions, you can review our guide on understanding business partnerships.

Choosing the right succession path is a significant decision with long-term consequences. The table below outlines key factors to help you evaluate your options.

Comparing Business Succession Pathways

| Succession Path | Primary Advantage | Key Consideration | Best Suited For |

|---|---|---|---|

| Family Transfer | Legacy & Continuity: Keeps the business within the family, preserving its name and values. | Family Dynamics: Requires fair treatment of all heirs and careful grooming of successors. | Owners whose top priority is maintaining a multi-generational legacy and have capable, willing family members. |

| Management Buyout (MBO) | Cultural Preservation: Rewards loyal employees and maintains the existing company culture. | Funding: The management team must be able to secure the necessary financing for the purchase. | Owners who want to ensure the company's ethos remains intact and wish to reward their leadership team. |

| Third-Party Sale | Maximum Liquidity: Often provides the highest financial return and a clean, decisive exit. | Loss of Control: The future direction, culture, and employee welfare are out of your hands. | Owners focused on maximizing their financial outcome for retirement or other ventures. |

The optimal choice is deeply personal, requiring an alignment of financial realities with your core values for the future of your company and your family.

Addressing the Human Element of Transition

While much focus is given to legal and financial structures, the most critical component of any successful transition is the people involved. A plan that appears sound on paper can falter if it does not account for the human element.

Thoughtful planning involves communicating your intentions with clarity and empathy. This means preparing the next generation of leaders, reassuring key employees about their future, and managing the expectations of family members. It is a process of building trust and consensus over time.

A succession plan is ultimately a story about the future. It must be a story that your family, your employees, and your leadership team can all see themselves in.

Unfortunately, many business owners postpone these important conversations. Survey data reveals a significant gap: 30% of owners have no succession plan at all. The same report found that nearly half (49%) of owners believe the next generation is only 'somewhat prepared' to handle the associated wealth and responsibility. These figures highlight the quiet urgency of beginning the process now.

By weaving your succession strategy directly into your estate plan, you transform a distant goal into a series of clear, manageable steps. This proactive approach provides control, reduces uncertainty for everyone, and honors the immense personal commitment you have made to your business.

Managing the Financial Mechanics of a Transition

Your succession strategy and legal documents form the blueprint of your estate plan. The financial mechanics—valuation, tax planning, and liquidity—are the engine that makes it function. Without careful attention to these details, even the most well-conceived plans can face challenges, creating pressure on your family and the business.

Addressing these financial elements is not about predicting the future but about building a resilient plan. This process begins with a crucial question: What is the business truly worth?

Establishing a Clear and Defensible Business Valuation

Before any meaningful decisions can be made, you need a reliable valuation. A formal, independent business valuation is the bedrock of effective estate planning for business owners. It is a defensible, detailed assessment of your company's fair market value conducted by a qualified professional.

This objective figure is critical. It sets a fair price for a buy-sell agreement, provides a baseline for calculating potential estate taxes, and helps ensure assets are divided equitably among your heirs. Planning without it is like navigating without a compass; it forces guesswork where precision is required.

An independent valuation transforms an abstract sense of worth into a tangible planning tool. It is the foundation upon which sound tax, succession, and estate strategies are built, replacing subjective opinion with objective fact.

The Critical Importance of Liquidity

Once you have a clear understanding of your business's value, the next conversation must address liquidity. In estate planning, liquidity refers to having sufficient cash—or assets that can be quickly converted to cash—to meet financial obligations without a forced sale of core assets. A significant obligation is often the estate tax, which is typically due within nine months of death.

If your estate lacks sufficient cash, your executor may be forced to sell company stock, real estate, or other important assets under pressure. Such a "fire sale" can diminish the value of the business and the inheritance you intend to leave. A prudent plan anticipates this need for cash and establishes a solution, often using life insurance to provide an immediate, tax-free source of funds when it is needed most.

Navigating Key Tax Considerations

Taxes are an unavoidable component of wealth transfer, but with proper strategy, they become manageable variables. For most business owners, the primary considerations are federal estate taxes and capital gains taxes.

- Estate Taxes: This tax is levied on the total value of your estate upon your death. Because your business is likely your largest asset, its valuation directly impacts your potential tax liability. Strategies such as gifting shares over time or moving ownership into certain types of trusts can help reduce the size of your taxable estate.

- Capital Gains Taxes: This tax applies to the appreciation of an asset when it is sold. The tax implications can vary significantly depending on whether the business is sold during your lifetime or inherited by your heirs. Inherited assets often receive a "step-up in basis," which can substantially reduce or even eliminate the capital gains tax liability.

The goal is to understand how these taxes function and to build a plan that addresses them strategically. A BNY Mellon Wealth Management report found that 40% of owners who sold their business wished they had commenced tax and estate planning sooner. They recognized that while their accountants were adept at annual filings, they needed specialized, long-term advice to preserve their legacy. You can find more details in the full report here.

This is where proactive financial and legal guidance becomes invaluable. By addressing the financial details in advance, you can make deliberate choices that balance your control today with your family's financial security tomorrow. For a primer on tax management, our guide on how to reduce taxable income can be a useful starting point. Demystifying the financials allows you to gain true command over your legacy.

Integrating Your Business Exit into Your Life's Financial Plan

An effective estate plan manages the technical details of a business transition, but its broader purpose is to secure your own financial independence and provide for your family, regardless of the company's future.

For most entrepreneurs, personal and business finances are closely linked. A crucial step in planning is to thoughtfully disentangle them, creating a clear distinction that ensures your family’s future is not solely dependent on the company’s performance.

This involves viewing your business exit strategy and your personal financial plan not as separate items, but as interconnected components of a single life plan. The objective is to build a personal wealth structure that is self-sustaining, integrating your investment portfolio, retirement income, and long-term tax strategy into one cohesive whole.

Building a Financial Firewall

Protecting your family’s security involves separating your personal wealth from the business long before a sale or transition. Think of this as creating a financial firewall.

Should the business encounter challenges or face litigation, this firewall ensures your personal assets—your home, retirement funds, and children's education savings—remain protected. This requires a mental shift from viewing the business as your sole safety net to treating it as one component of a larger, diversified financial picture. It is a disciplined approach that yields something invaluable: peace of mind.

True financial peace of mind is not derived from a single successful quarter or a major contract. It comes from knowing your personal security is no longer tied to the business cycle. It is the confidence that comes from your life's work funding a future that is stable, clear, and truly yours.

Your Financial Quarterback: The Fiduciary Advisor

Coordinating this complex process requires a skilled professional who can act as the architect for your entire financial life. A fiduciary advisor serves in this role, ensuring all disparate parts work in harmony. Their duty is to provide objective guidance, helping you make decisions that align your business transition with your personal life goals.

This coordinated approach includes:

- Defining Financial Independence: An advisor helps quantify your goals, calculating the specific capital required from the business to fund the life you envision, rather than relying on a vague notion of "retiring comfortably."

- Synchronizing Timelines: They work with you to align the timeline for your business succession with your personal retirement plan, ensuring capital is available when you need it.

- Integrating Tax Strategy: A unified plan considers the tax implications of both the business sale and your personal income strategy, with the objective of preserving as much of your wealth as possible.

This level of integrated planning synthesizes your will, trusts, buy-sell agreement, and personal investments into a single, coherent strategy. Having a well-conceived plan for your next chapter is essential, and you can gain further perspective by exploring our guide on retirement planning.

Ultimately, this process is about more than financial metrics. It is about confidently transitioning to the next stage of your life, knowing the legacy you built has created a lasting foundation for you and those you care about.

Beginning Your Estate Planning Journey

Initiating the estate planning process can feel like a significant undertaking. However, the first step is not legal paperwork; it is personal clarity. The most effective plans are built on a foundation of well-considered personal goals. Before engaging experts, take time to reflect on the core questions that will guide every subsequent decision.

What does "legacy" truly mean to you? Is it defined by financial assets? Or is it about family unity, community impact, or the preservation of your company’s unique culture? Defining your answer provides a guiding principle for your entire strategy. Once you have a clear vision for your ideal future, the technical details of the plan can be addressed more effectively.

Assembling Your Advisory Team

No single advisor can manage this process alone. Estate planning for a business owner is a collaborative effort, relying on a team of specialists who each contribute a distinct and crucial perspective.

Your core team will generally include these three key professionals:

The Estate Planning Attorney: This is your legal architect. They draft the critical documents—your will, trusts, and powers of attorney—that form the plan's structure. Their role is to translate your vision into legally sound instructions.

The Certified Public Accountant (CPA): Your CPA serves as your tax strategist. They analyze the financial data and model various scenarios to illustrate the tax implications of your choices, helping you navigate estate, gift, and capital gains taxes.

The Fiduciary Financial Advisor: This professional acts as the coordinator, ensuring that all components of your financial life—your business succession plan, personal investments, retirement goals, and insurance—are integrated into a cohesive strategy. They connect the legal and tax elements to your real-life objectives.

The purpose of assembling this team is not simply to receive answers, but to engage in a strategic conversation. The right team does not just provide directives; they empower you by clarifying complexities, giving you the confidence to make informed decisions for yourself and your family.

At its core, estate planning for business owners is an act of stewardship. It is not a one-time task but a living plan that will evolve with your life, your family, and your business. By starting with thoughtful reflection and gathering the right experts, you can transform a daunting project into a deeply rewarding one—securing not just your wealth, but your peace of mind.

Frequently Asked Questions

It is natural to have questions when planning for the future of your business. Here are answers to some of the most common inquiries from entrepreneurs.

When Is the Right Time to Start Estate Planning for My Business?

The ideal time to begin is now. Effective planning is a process, not a singular event.

Starting early, regardless of your age or the maturity of your business, allows you the time to structure agreements, consider tax implications, and prepare successors without the pressure of an unexpected health issue or other urgent event forcing a hasty decision.

What Is a Common Mistake Business Owners Make?

One of the most consequential oversights is the failure to create and properly fund a Buy-Sell Agreement. While it sounds technical, its absence can lead to significant disruption.

Without this document, your partners or heirs are left without a clear process for valuing or transferring your ownership stake. This often results in disputes, forced sales at unfavorable prices, and, in some cases, can jeopardize the continuity of the business. A clear agreement removes ambiguity during an already challenging time.

Most business transitions are not seamless. The median sale price for small businesses that find a buyer is approximately $315,000. For family businesses, the data is also sobering: nearly two-thirds lack a written succession plan, placing their legacy at risk. You can explore more of these business owner exit planning statistics to understand the importance of proactive planning.

How Does a Trust Help Protect My Business and Family?

A trust can be viewed as a legal structure that separates your business assets from your personal estate. This separation offers several key benefits.

It can help your heirs avoid the lengthy and public probate court process. A trust can also provide a degree of protection for assets from creditors, help minimize estate taxes, and ensure your business is transferred to your chosen successor according to your specific instructions.

Can I Change My Estate Plan After It Is Created?

Yes. Most core estate planning documents, such as a Will and a Revocable Living Trust, are designed to be flexible. Life is dynamic, and your plan should adapt accordingly.

You can and should review your plan as your business grows, your family situation changes, or your personal objectives evolve. While certain instruments, like Irrevocable Trusts, are designed to be permanent, the majority of your plan is adaptable. Regular reviews with your advisory team are recommended to ensure your plan continues to reflect your wishes.

Securing your financial future and protecting your business legacy begins with a clear, actionable plan. At Wealth Accel, we specialize in helping business owners integrate their personal and professional financial worlds.

Let's discuss how our fiduciary guidance can bring clarity and confidence to your next chapter.

Learn more and schedule your complimentary introduction at Wealth Accel

Published via Outrank